It’s time to tax aviation more

29th October, 2024

{kind=link}

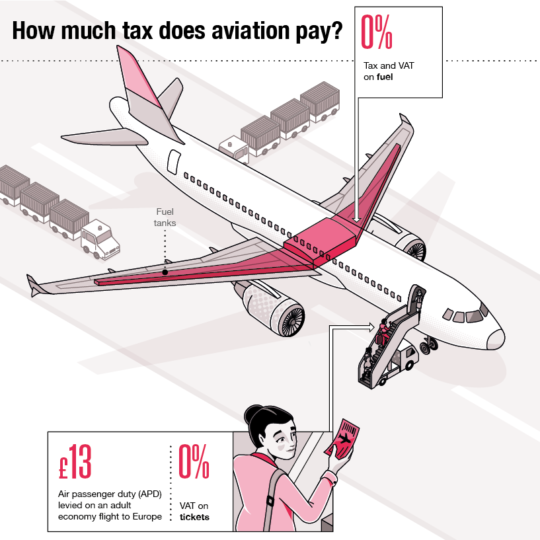

Historically, the aviation industry has benefitted from many tax breaks. Even now, no fuel duty is paid on jet fuel, and no VAT is applied. This irregularity becomes harder to explain when we look at how tax is applied to other transport modes. When compared to car travel, for example, aviation’s exemption from fuel duty and VAT appears more like an indirect subsidy that allows airfares to be kept artificially low. The absence of tax has helped to fuel passenger growth and the sector’s CO2 emissions have increased 125% since 1990. Over the same period, the UK’s overall emissions decreased by 43%.

Plane versus car

Currently, the only tax levied on air travel is Air Passenger Duty (APD), which is paid by passengers, not airlines. No duty or VAT is paid on aviation fuel. If aviation did pay taxes equivalent to motorists it would raise a further £7.5 billion for the Exchequer (on top of the £4 billion already collected through APD).

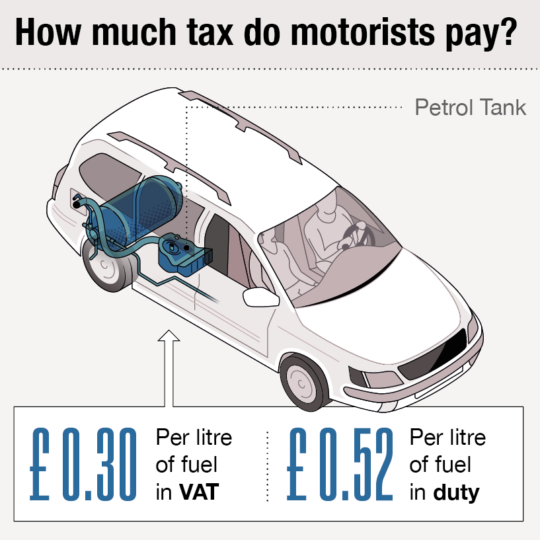

Road fuel duties are currently levied at just under 52.95p and are expected to raise £24.7 billion in tax revenue in 2023-4.

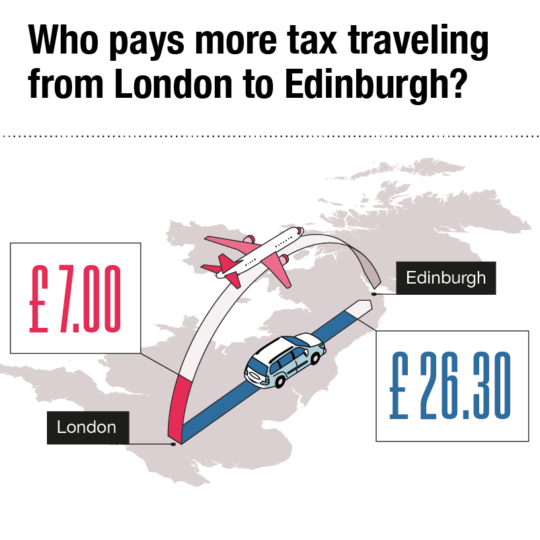

This disparity in taxes creates unfair advantages. Using a journey from London to Edinburgh as an illustration, a passenger choosing to make the trip by car would pay nearly four times as much in tax compared to flying.

It is also worth mentioning that these exemptions are at odds with the need to encourage a shift to less carbon-intensive modes of transport, such as the train. In fact, some organisations are campaigning for raising taxes on aviation and using the funds to provide cheaper rail fares.

How can we tax aviation more?

The simplest way to tax aviation more is to increase Air Passenger Duty. It already accounts for seating class and length of flight (although further distance bands could be added), and is straightforward to administer and collect.

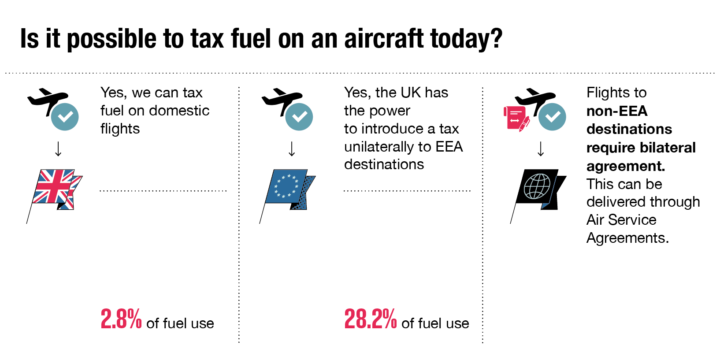

But exempting aircraft fuel from tax remains an anomaly. Many people believe that aviation cannot be taxed because of provisions in the Chicago Convention, signed in 1944 and which established the International Civil Aviation Organisation as a specialised agency of the United Nations. This is not true. Fuel already onboard planes cannot be taxed, but there is no ban on taxing the fuel uplifted in any country. The obstacle lies in the multitude of Air Service Agreements (bilateral agreements between states that govern how aviation operates between those countries/regions). Currently, most ASAs are interpreted as prohibiting their signatories from levying a fuel tax on international flights without the consent of both parties. But fuel duty can be applied to kerosene for domestic flights and the ASA negotiated between Europe and the UK after the latter left the European Union, allows the UK to impose a tax on the fuel used on routes to EEA destinations. This could be done without fear of widespread tankering – airlines filling up at non-UK airports – because EU regulation requires the majority of fuel to be uplifted at the airport of departure.

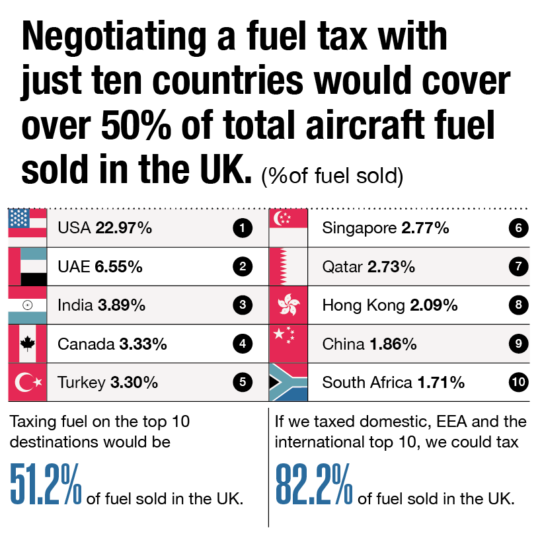

Through bilateral negotiations the UK and like-minded partners could create a system to tax kerosene. In fact, negotiating a fuel tax through ASAs with just ten non-EEA countries would cover over 50% of total aircraft fuel sold annually in the UK.

Taxing domestic fuel, and fuel for flights to EEA destinations plus the top ten non-EEA destinations, would cover an estimated 82.2% of UK aircraft fuel sales.

Aviation should pay for its externalities

The concept of externalities is defined as an industry’s indirect cost or benefit that is not captured by the market price. Specifically for aviation, negative externalities include impacts on climate, and public health impacts through air pollution and aircraft noise.

The aviation industry would argue that its inclusion in the UK Emissions Trading Scheme (ETS) means that it is paying a price for its carbon emissions. It is also worth noting that ICAO, a specialised UN agency, has an offsetting system called CORSIA. Both of these schemes could be said to somewhat enable aviation to begin to pay for its carbon emissions. However, in reality, a combination of free allowances and a generous activity threshold before airlines need to start offsetting, means that only around 16% of the carbon abatement costs associated with airport expansion are currently captured by these schemes.

Raising taxes on kerosene could be considered as another way to reflect these negative externalities. As emphasised by the polluter pays principle (Rio Convention, 1992), those responsible for pollution should bear the cost of managing it, to avoid damage to human health and the environment.

So how can we tax aviation more?

- Government should increase APD immediately (timescale: immediate)

- Government should apply a tax and VAT on aviation fuel used on domestic flights (timescale: immediate)

- Government should apply duty and VAT to the fuel used on routes to EEA destinations (timesacle: immediate)

- By 2030 Government should seek to reach agreement with the top 10 non-EEA states to introduce duty and VAT, extending that to the top 25 states by 2040, and with all states as and when all remaining ASAs are renegotiated

- Government should explore the feasibility and practical implementation of other tax measures that take distributional impacts into account (70% of flights are taken by just 15% of the UK population), such as an air miles or frequent flyer levy