Government looks to carbon offsets to meet aviation net zero commitments in new climate plan

25th November, 2025

Overview

- Recognising carbon offsets from ICAO’s CORSIA now makes up the second largest emissions savings of any aviation policy from 2033-2037 (2.8MtCO2/year) in the Government’s new Carbon Budget and Growth Delivery Plan.

- Total emissions reductions for aviation from 2033-2037 have more than doubled between the 2023 and 2025 plans from 5.5 to 11.45 Mt/year CO2e due to increased contributions from ‘sustainable’ aviation fuels (SAF), CORSIA offsets, carbon pricing and efficiency.

- Information on how these reductions will be achieved is limited, with no updated forecasts or modelling provided.

- There is no longer any reference to the Jet Zero strategy (2022) and quantification of one of policies, influencing consumers, has also been removed.

Last month, the Government published the much anticipated Carbon Budget and Growth Delivery Plan (CBGDP). The CBGDP is a report required by the Climate Change Act that outlines policies to reduce emissions up until 2037. These policies are designed to meet the next three carbon budgets (CB), which set limits over five year periods on the amount of carbon that the UK can emit (see Table 1). The CBGDP is an update to the 2023 delivery plan, which the High Court ruled was too reliant on ‘unproven and high-risk technological fixes’.

Is the new Carbon Budget and Growth Delivery Plan good enough?

In terms of overall emission reductions, the CBGDP does now meet the requirements of all three of the carbon budgets, something the 2023 version failed to do by falling short of CB6 and relying on unquantified, uncertain savings. The plan has gained credit for reinforcing climate commitments at a time when they are under increasing political pressure. However, general reaction has been fairly low-key, with much of the plan outlining existing policy commitments and concerns being raised over whether it is ambitious and robust enough. Given that CB7 (from 2038 to 2042) has to be legislated by June 2026, and will be accompanied by another delivery plan, there is a sense that the CBGDP has lost some of its significance, functioning more as a policy snapshot that is largely only important for the next year.

What are the key aviation policies of the Carbon Budget and Growth Delivery Plan?

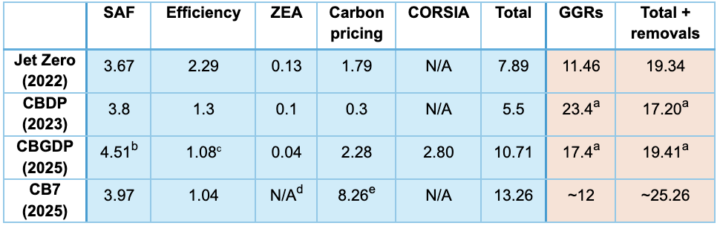

The core policies remain sustainable aviation fuel (SAF), carbon pricing, fuel efficiency savings and zero emission aviation (ZEA), with the SAF mandate still the headline tool for decarbonisation. There is a greater emphasis on engaging internationally with the International Civil Aviation Organisation (ICAO), including recognising offsets purchased under ICAO’s Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA) in CB6. This goes against the advice of the Climate Change Committee which argued against inclusion until CORSIA undergoes significant reform. Meanwhile, quantifying the impact of Jet Zero’s commitment to provide consumers with environmental information when booking flights has been removed. Although not explicitly tied to aviation, greenhouse gas removals (GGRs) are also a key part of the Government’s strategy for the sector. Table 2 (below) compares the emissions reductions across CB6 for policies from the Jet Zero strategy, both carbon budget delivery plans and the Climate Change Committee’s (CCC’s) report on the Seventh Carbon Budget (CB7).

aGGR figures for the CBDP and CBGDP are for the whole economy – we have assumed that aviation will use ½ of the available GGRs for the ‘total + removals’ column

bCBGDP SAF reduction figure includes some unpublished savings from fuel efficiency

cEfficiency figure reduced by 0.82 Mt as per Secretary of State statement in Feb 2026

dZEA in CB7 is included in the efficiency figure

eThe carbon pricing figure for CB7 covers demand management which includes reductions in demand from price increases from the ETS and CORSIA and the implementation of new technology (e.g. SAF and removals)

Total savings per year for CB6 have more than doubled between the 2023 and 2025 delivery plans, going from 5.5 Mt CO2e/year to 11.45 Mt CO2e/year, with most of this increase is from carbon pricing and the inclusion of offsets from CORSIA. Combined savings for aviation policies across all years (2023-2037) have also increased from 47 to 91 Mt.

- CORSIA and Carbon Pricing

The addition of offsets from CORSIA, entirely ‘out of sector’, is surprising given that they have not previously appeared in previous government delivery plans or the Jet Zero Strategy. There is also a substantial increase in savings from carbon pricing between the 2023 and 2025 plans from 0.3 to 2.28Mt/year across CB6. Although no new carbon price modelling is provided, this change is likely to be due to updates to DESNZ carbon pricing forecasts as there has been no change to the scope of the UK ETS in relation to aviation.

Carbon pricing incentivises decarbonisation by charging for emissions (via both the UK Emissions Trading Scheme (ETS) and CORSIA). Both pricing mechanisms have flaws, with the UK ETS currently only covering roughly ¼ of UK aviation emissions and prices forecast to be well below those assumed in the Jet Zero strategy. CORSIA prices are even lower and there are additional question marks over what will happen to the scheme after 2035 when it is currently scheduled to end – midway through CB6. The government’s climate advisors, the Climate Change Committee, strongly recommend against these international credits being used for compliance in carbon budgets.

- SAF, Efficiency and ZEA

Estimated SAF savings have increased between Jet Zero, 2023’s Carbon Budget Delivery Plan (CBDP) and the CBGDP, now reaching 4.51 Mt/year across CB6. These changes are likely due to updates to the accounting methods used as the trajectory for SAF deployment is now well established, and there have not been any major breakthroughs on supply or the sustainability of sustainable fuels.

Efficiency savings have increased from the CBDP but are still below the projected savings from Jet Zero which were based on an average improvement of 2% per year from 2017 to 2050. This could be due to a decrease in projected efficiency savings or other factors such as knock-on effects from the Covid-19 pandemic delaying efficiency measures. Although airspace modernisation is mentioned, there is still yet to be any public information on the impact this is expected to have on emissions. ZEA continues to make a very small contribution to emissions reductions over the CB6 period.

- What role do engineered carbon removals play?

The other key policy lever relevant to aviation is engineered GGRs, covering technologies that remove carbon directly from the atmosphere or during industrial processes. It is expected that aviation will use up a large proportion of GGRs (e.g. the CCC allocated ~60% of removals in 2050 to aviation in CB7). Whilst estimates of the sector’s need for emissions reductions from GGRs have fallen from the 2023 plan, the 17.4 Mt/year across CB6 is still hugely ambitious and risky, given that to date all available plans for engineered removals in the UK total less than 1 Mt/per year.

Where does this leave aviation?

In some ways the position of aviation is uncertain and in others it’s very simple. All references to the Jet Zero strategy and one of its key policies (consumer information) have been removed in the new CBGDP, making it unclear whether the strategy is still fully applicable. Other than the emissions savings figures, there is no new published modelling, with the plan ignoring recent Jet Zero projections and referring back to DfT’s 2017 UK Aviation Forecasts. It is now expected that new evidence to 2050 (and beyond) will be produced as part of the Airports National Policy Statement review. The current lack of published forecasting of emissions or passenger numbers makes it difficult to assess how airport expansion fits into the picture, with the CBGDP simply stating that: ‘DfT modelling accounts for the estimated impact on demand of all known airport expansion plans – mitigating risk that demand will exceed projections.’ This statement, alongside unexplained increases in savings across the aviation policy mix, raises more questions than it answers.

What is clearer is that while carbon savings can be modelled over and over, real assessment of the environmental credentials of aviation policy may only happen when the sector drifts off track, with increasing passenger numbers and a reliance on unproven technology risking the under-delivery of emissions cuts. There is little evidence of contingency planning to correct any deviations from planned trajectories, with the additional mitigation of demand management, repeatedly highlighted by the CCC as the key policy for addressing aviation emissions, receiving no mention in the CBGDP (except, indirectly through carbon pricing impacts on ticket costs).

Whilst technically still official government policy, the removal of references to Jet Zero leaves the strategy neither endorsed nor rejected, with the relevance of different policies and modelling unclear. The lack of new published demand and emissions forecasting adds to the sense that net zero aviation policy to 2050 is incomplete, with the CBGDP not fully addressing how the major challenges for decarbonising aviation will be met.

For wider analysis of the CBGDP, see these pieces from Carbon Brief, EDRC and Friends of the Earth, who were one of the organisations that took the previous plans to court.